What Is a Medicare Supplement Plan? Types, Costs, and How to Choose

Navigating the landscape of healthcare after retirement can feel like deciphering a complex puzzle. While Original Medicare provides a solid foundation, it often leaves beneficiaries with significant “gaps” in coverage—unpredictable out-of-pocket costs that can threaten financial stability.

As Dr. Julian, I have spent years helping seniors understand how their insurance choices impact their actual medical care. I recently interviewed a patient named Robert, a 68-year-old retired teacher who was blindsided by a $4,000 hospital bill despite having Medicare Part A.

Robert’s experience is common; he assumed “Medicare covered everything.” After we sat down to review his options, he transitioned to a Medicare supplement insurance plan. He later told me that the peace of mind knowing his “gaps” were filled was worth every penny of the monthly premium.

This guide will explain what a Medicare supplement plan is, how these policies function in 2026, and how to choose the right lettered plan to protect your health and your savings.

Medicare Supplement Plan Definition

To understand what Medicare supplement insurance is, you must first view it as a secondary layer of protection. These policies, also known as Medigap, are sold by private insurance companies rather than the federal government.

A Medicare supplement insurance plan is specifically designed to “fill the gaps” left by Original Medicare (Part A and Part B). When you receive a medical service, Medicare first pays its share of the approved amount. Then, your Medigap policy steps in to pay its share, which usually includes your deductibles and coinsurance.

It is important to clarify that you must have Medicare Part A and Part B to buy a supplement. Furthermore, these plans are strictly individual. If both you and your spouse want coverage, you must each buy separate policies.

In 2026, Medigap remains a favorite for retirees because it offers freedom. Unlike managed care plans, a supplement allows you to see any doctor or specialist in the country who accepts Medicare, without needing a referral.

What Does a Medicare Supplement Plan Cover?

When asking what a supplement plan in Medicare is used for, the answer lies in the “hidden” costs of healthcare. Original Medicare typically covers 80% of Part B expenses, leaving you responsible for the remaining 20%.

A Medigap policy typically covers:

- Medicare Part A Coinsurance: Hospital costs for up to an additional 365 days after Medicare benefits are exhausted.

- Medicare Part B Coinsurance: The 20% of the bill that Medicare doesn’t pay for doctor visits and outpatient services.

- Blood: The first three pints of blood needed for a medical procedure.

- Skilled Nursing Facility Coinsurance: Help with the daily costs of recovery in a specialized facility.

However, it is equally important to know what they do not cover. Medicare Supplement plans generally do not include coverage for dental, vision, hearing aids, or long-term care (nursing homes).

Most notably, they do not include prescription drug coverage. In my experience, I always advise patients to pair their Medigap plan with a standalone Medicare Part D plan to ensure their medications are affordable.

Types of Medicare Supplement Plans (A–N)

Medicare Supplement plans are standardized by the government, meaning every “Plan G” offers the exact same benefits, regardless of which insurance company sells it. There are currently 10 standardized plans available in most states, labeled A through N.

The Medicare supplement plans comparison chart usually highlights the most popular options: Plans F, G, and N. Each lettered plan offers a different level of “gap filling.” Plan A offers the most basic coverage, while Plan G and Plan F are the most comprehensive.

Choosing between them is a balancing act between monthly premiums and out-of-pocket risk. For example, some plans cover your Part A deductible (the cost to enter a hospital), while others require you to pay a portion of the bill in exchange for a lower monthly rate.

In 2026, the top 5 Medicare supplement plans based on enrollment are Plan G, Plan N, Plan F, Plan D, and Plan M. Understanding the nuances of these letters is the key to not overpaying for coverage you don’t need—or under-buying and facing a surprise bill.

What Is a Medicare Supplement Plan? G?

If you are looking for the most popular supplement plan for Medicare for new enrollees, Plan G is the clear winner. Since 2020, it has become the “gold standard” for those who want the highest level of coverage available to them.

What is a Medicare Supplement Plan G? It covers every single gap in Original Medicare except for one: the Part B annual deductible. Once you have paid that relatively small deductible (which is $257 in 2026), Plan G covers 100% of your remaining Medicare-approved medical expenses for the rest of the year.

The reasons people choose Plan G include:

- Predictability: You know exactly what your medical costs will be for the year (premium + Part B deductible).

- Foreign Travel: It provides emergency medical coverage during international trips.

- No Copays: Unlike Plan N, there are no small copayments for office visits or ER trips.

From a clinical perspective, I see the most “financial stress-free” patients in the Plan G category. They never hesitate to see a specialist because they know the bill is already taken care of.

What Is a Medicare Supplement Plan? F?

Historically, Plan F was the “Cadillac” of Medigap. What is a medicare supplement plan f? It is the only plan that covers 100% of all Medicare gaps, including the Part B deductible. With Plan F, you literally never see a medical bill for Medicare-approved services.

However, there is a major catch: Plan F is no longer available to people who became eligible for Medicare after January 1, 2020. If you were already on Medicare before that date, you can keep your Plan F or even switch to a different company’s Plan F.

While it offers total peace of mind, the premiums for Plan F are often significantly higher than those for Plan G. In many cases, the extra premium you pay for Plan F is more than the cost of the Part B deductible itself, making Plan G a better mathematical value for many.

What Is a Medicare Supplement Plan? N?

For those who are healthy and want to save on monthly premiums, what is a medicare supplement plan n? Plan N is a “mid-range” option that offers lower premiums in exchange for a bit of cost-sharing.

With Plan N, you still get excellent coverage for major hospital stays and Part B coinsurance, but you are responsible for:

- The Part B annual deductible.

- Copayments of up to $20 for some office visits.

- A copayment of up to $50 for emergency room visits (waived if you are admitted).

- “Part B Excess Charges” (though these are rare and illegal in some states).

Plan N is an excellent choice for retirees who don’t visit the doctor frequently but want protection against catastrophic hospital bills. It offers the same nationwide network and freedom as Plan G but at a more affordable monthly price point.

What Is Medicare Supplement Plan C?

Similar to Plan F, what is a Medicare Supplement Plan C? It is a comprehensive plan that covers the Part B deductible. Like Plan F, it was phased out for new beneficiaries in 2020 to discourage over-utilization of healthcare services.

Plan C covers almost everything Plan F does, except for Part B excess charges. If you are a “newly eligible” senior in 2026, you won’t be able to purchase Plan C. If you are an older beneficiary still holding a Plan C policy, you may find that your premiums are rising faster than Plan G as the pool of enrollees in Plan C gets smaller and older.

Average Cost of Medicare Supplement Plans

When budgeting for retirement, you must ask: What is the average cost of a Medicare supplement plan? Because these are private plans, prices vary significantly based on your age, gender, tobacco use, and zip code.

In 2026, the typical monthly premium ranges are

- Plan G: $140 – $280 per month.

- Plan N: $90 – $180 per month.

- High-Deductible Plan G: $40 – $80 per month.

It is also vital to understand how companies price their plans. Some use “Community Rated” pricing (everyone pays the same), while others use “Attained Age” pricing (your premium increases as you get older).

I always tell my patients to look beyond the “introductory” price. A company might have the cheapest Plan G today, but if they have a history of 15% annual rate increases, they could be the most expensive option in five years.

Why Get Medicare Supplemental Insurance?

You might wonder, with all these premiums, why get Medicare supplemental insurance at all? The answer is “financial certainty.” Original Medicare has no “out-of-pocket maximum.”

If you have a catastrophic illness and a $200,000 hospital bill, the 20% coinsurance would leave you with a $40,000 debt. A Medigap plan places a “cap” on your liability.

Beyond the money, it offers access. With a supplement, you aren’t trapped in an HMO network. If the best specialist for your condition is three states away, you can go see them as long as they take Medicare. For many of my patients, that freedom is the most valuable part of the plan.

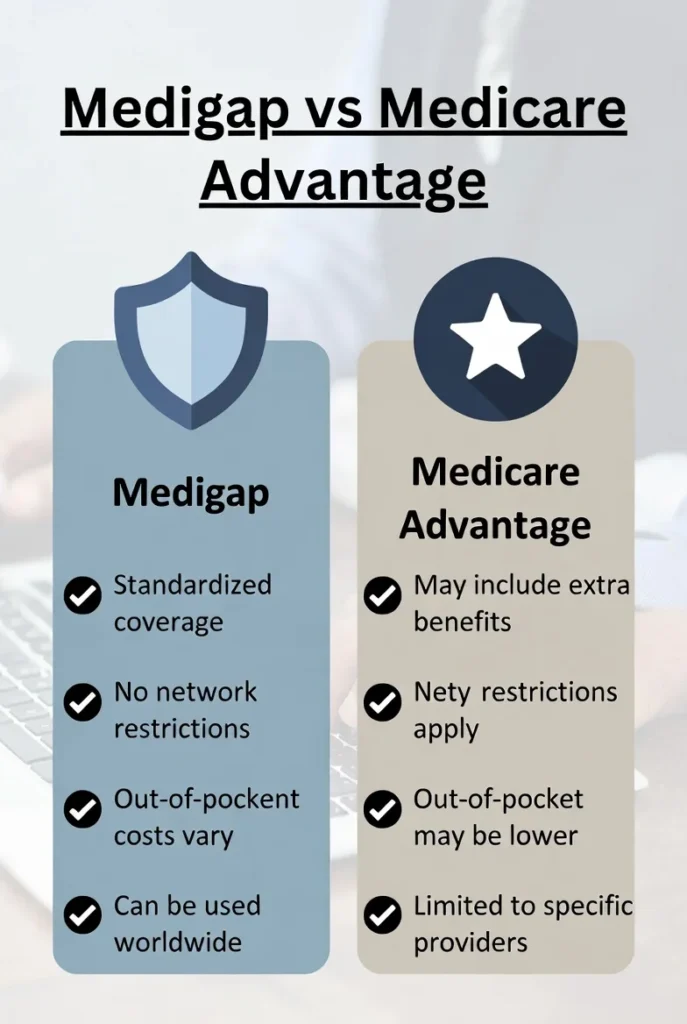

Medigap vs Medicare Advantage

The biggest fork in the road for seniors is Medicare vs. Medicare Advantage. They are fundamentally different ways of receiving your benefits.

- Medicare Supplement (Medigap): Works with Original Medicare. It has higher premiums but lower out-of-pocket costs and no network restrictions.

- Medicare Advantage (Part C): Replaces Original Medicare. It often has $0 premiums and includes dental/vision/drugs, but it uses restricted networks (HMO/PPO) and requires copays for every service.

Choosing Medigap is like buying “pre-paid” healthcare. Choosing Advantage is “pay as you go.” If you prefer to know exactly what your costs are and want to see any doctor, Medigap is usually the superior choice.

Choosing the Best Medicare Supplement Plan

Choosing medicare supplemental insurance plan requires an honest look at your health and your checkbook. If you visit the doctor frequently or have a chronic condition, Plan G is almost always the “best” plan because it eliminates almost all variable costs.

If you are “doctor-averse” and only go in for your annual checkup, Plan N or even a high-deductible Plan G can save you thousands in premiums over a decade.

I recommend getting quotes from at least three different Medicare supplement insurance companies. Since the benefits are identical by law, you are essentially shopping for the lowest price and the most stable company reputation.

Frequently Asked Questions

What is the difference between Medicare and Medicare Supplement plans?

Medicare is the primary insurance provided by the government. A Medicare Supplement plan is private insurance that pays for the deductibles and coinsurance that Medicare leaves behind.

What is the most popular supplement plan for Medicare?

Currently, Plan G is the most popular choice for new enrollees because it offers the most comprehensive coverage available to those eligible after 2020.

What are the disadvantages of Medicare Supplement plans?

The main disadvantages are the monthly premiums (which you pay even if you don’t use medical services) and the fact that they do not include prescription drug, dental, or vision coverage.

What is the average monthly cost of a Medicare Supplement plan?

Most beneficiaries pay between $120 and $250 per month, depending on their location, age, and the specific lettered plan they choose.

What is a Medicare Supplement Plan? F?

Plan F is a “full-coverage” plan that pays for all Medicare gaps, including the Part B deductible. It is only available to those who were eligible for Medicare prior to January 1, 2020.

Conclusion

Navigating the transition into Medicare is one of the most significant financial milestones for any retiree. As we’ve explored, Original Medicare is a robust foundation, but its lack of an out-of-pocket maximum makes “gap” coverage a necessity rather than a luxury.

Whether you choose the all-encompassing protection of Plan G or the premium-conscious structure of Plan N, the primary goal remains the same: transforming unpredictable medical bills into a manageable monthly budget.

As I saw with my patient Robert, the real value of a Medicare Supplement plan isn’t just found in the dollars saved on hospital coinsurance; it’s found in the freedom to choose any doctor in the country and the elimination of “bill shock” after a health crisis.

In 2026, with the Part B deductible rising to $283, having a plan that covers the remaining 20% of your outpatient costs is more critical than ever for maintaining long-term financial health.

Before you make a final decision, take a moment to review your projected health needs for the coming year. If you value total predictability, Plan G is your best ally.

If you are in good health and want to minimize your fixed costs, Plan N offers a sophisticated alternative. Whatever you choose, ensuring you are enrolled during your Medigap Open Enrollment Period is the single best way to lock in the best rates for life.

References

Related Posts

MORE from Author

Read More Just last week, a patient named Sarah walked into my clinic carrying three different boxes of popular gut biome tests.…

Just last week, a patient named Sarah walked into my clinic carrying three different boxes of popular gut biome tests.… Recently, a frustrated patient named Mark visited my public health clinic. He handed me an expensive, beautifully packaged at-home stool…

Recently, a frustrated patient named Mark visited my public health clinic. He handed me an expensive, beautifully packaged at-home stool…

- Have you ever felt constantly exhausted and painfully bloated after normal meals? Recently, a patient named Sarah sat in my…

It's scary to wake up in the middle of the night and not be able to move or talk. People…

It's scary to wake up in the middle of the night and not be able to move or talk. People…